Cheque Bounce Law in India - Overview & Practice

Cheque bounce is one of the most frequently litigated financial offences in India. Despite the digital revolution, cheques remain a preferred mode of financial assurance, particularly in business and lending transactions. However, with over 35 lakh cases pending across Indian courts, understanding the legal framework and your rights in cheque bounce cases is crucial.

What is Cheque Bounce under Indian Law?

A cheque is said to have bounced when it is returned unpaid by the bank due to reasons such as insufficient funds, account closure, signature mismatch, or payment stopped by drawer. Under Section 138 of the Negotiable Instruments Act, 1881, cheque bounce is a criminal offence punishable with imprisonment of up to 2 years, or a fine up to twice the amount of the cheque, or both.

Essential Ingredients:

Cheque must be drawn on an account maintained by the drawer.

It must be issued for the discharge of a legally enforceable debt or liability.

It must be presented within its validity period (3 months).

The bank must return the cheque unpaid.

A written demand notice must be sent within 30 days of dishonour.

Drawer must fail to pay within 15 days of receiving notice.

Complaint must be filed within 30 days of expiry of notice period.

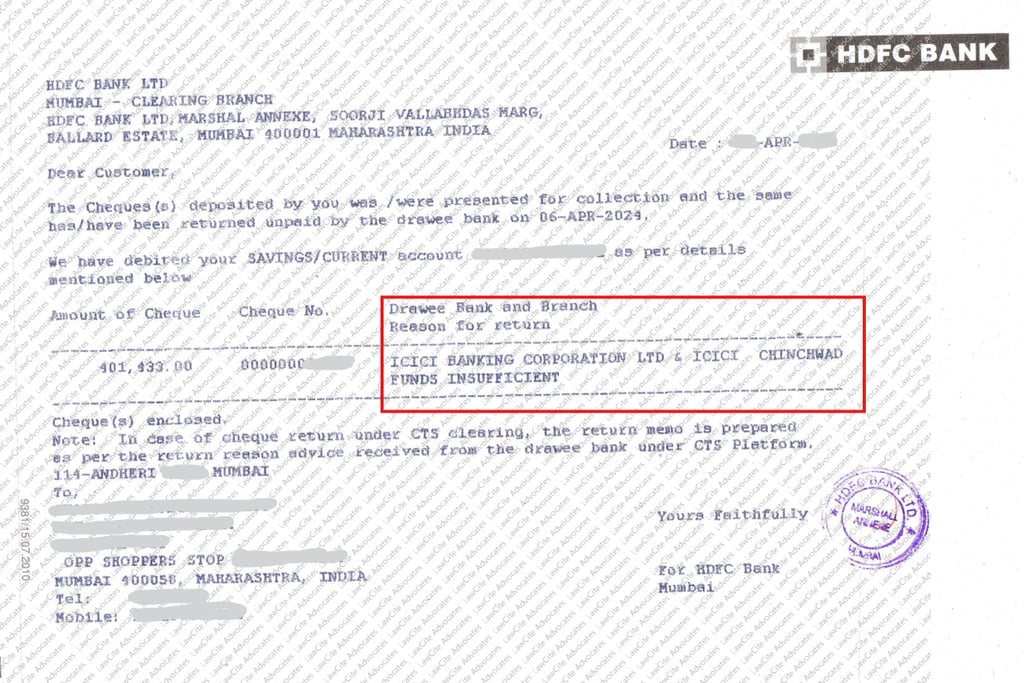

A crucial document in proving cheque dishonour is the bank return memo. This memo, issued by the drawee bank, contains the specific reason for which the cheque was returned unpaid such as 'insufficient funds', 'account closed', 'payment stopped by drawer', or 'signature mismatch'. The return memo not only authenticates the fact of dishonour but also forms the basis for sending the legal notice to the drawer. Courts consider it essential evidence and it must accompany the complaint when filing the case under Section 138.

Legal Procedure for Filing a Cheque Bounce Case

Step-by-Step:

Issue a legal notice to the drawer within 30 days.

Wait for 15 days. If no payment is made, file a criminal complaint within the next 30 days.

The complaint must be filed at the court where the cheque was presented.

Complainant must file the original cheque, bank memo, copy of notice, proof of delivery, and supporting documents.

Summons will be issued to the accused.

Trial follows: evidence, cross-examination, final arguments, judgment.

Corporate and Director Liability

In the case of cheques issued by companies or firms, not only the company but also the directors, officers, and authorised signatories may be held liable under Section 141 of the NI Act.

However, independent directors or non-executive directors are not automatically liable unless specific allegations show their involvement in day-to-day affairs.

Complaint must name the company and include those directors/officers responsible for business conduct. Notice to the company is mandatory; notice to directors is not required.

Key Defences for the Accused

Cheque given as Security: If the cheque was not issued against an existing debt or liability.

Stop Payment Instruction: Can be a valid defence if the drawer had sufficient funds and stopped payment for legitimate reasons.

No Enforceable Debt: If no contract, delivery, or obligation was due.

Lost/Stolen Cheque: If the drawer reports the cheque as stolen and has FIR proof.

Compromise-based Cheques: If issued as part of a compromise without underlying debt.

Special Scenarios Recognised by Courts

Cheque issued in settlement (Lok Adalat or compromise): Still liable if legal liability exists.

Post-dated cheques: Valid if issued against future liability.

Signature mismatch: Still covered under Section 138.

Cheque presented twice: Second dishonour is prosecutable if notice timeline is followed.

Proceedings under IPC (406, 420): May proceed alongside NI Act if mens rea is proven.

Interim Relief & Compensation

Under Section 143A of the NI Act (Amendment, 2018):

Magistrates may direct the drawer to pay up to 20% of cheque amount as interim compensation.

If acquitted, the complainant must refund the amount with interest.

Under Section 148:

Appellate courts may direct deposit of minimum 20% of fine/compensation during appeal.

Cheque Bounce and Insolvency Proceedings

As per the Supreme Court ruling in P. Mohanraj v. Shah Brothers Ispat, once a company is undergoing insolvency under the IBC, 2016, proceedings under Section 138 of NI Act against the company are barred. However, directors and signatories may still face prosecution.

Out-of-Court Settlement (Compounding)

Cheque bounce offences are compoundable:

Parties can settle at any stage.

Court may impose costs depending on delay:

0% if settled before first hearing

10% at Magistrate level

15% at Sessions/High Court

20% at Supreme Court

Even if the complainant refuses, the court may allow compounding in appropriate cases to reduce judicial burden

Advocate Vipin Sharma is an enrolled legal practitioner handling cheque dishonour disputes, including matters under Section 138 of the Negotiable Instruments Act. His practice involves representing both parties initiating complaints and those responding to them.

He provides legal support to clients in:

Drafting statutory legal notices

Filing and defending Section 138 complaints

Managing timelines and procedural compliance

Advising on enforceability, settlement, and compounding

Supporting parallel civil recovery where applicable

For the Complainant:

To initiate valid legal proceedings:

The cheque must be issued for a legally enforceable debt or liability.

It must be presented within the validity period.

A legal notice must be sent within 30 days of dishonour.

The drawer must be given 15 days to make payment.

Complaint must be filed within 30 days after the 15-day period expires.

Proper documentation such as the original cheque, return memo, copy of legal notice, and delivery proof is essential.

For the Accused:

The presumption under Section 139 is rebuttable. Valid defences include:

Cheque issued only as security

No legally enforceable liability

Misuse or unauthorised use of cheque

Payment already made

Procedural lapses such as improper notice

Courts require documentary proof or credible evidence to accept these defences.

Compounding and Settlement

Section 138 offences are compoundable. Settlement can occur at any stage with mutual consent.

Once compounded, proceedings end and the accused is acquitted.

The court may impose a cost depending on the stage of compounding.

Withdrawal of complaint is allowed if payment is made before or during proceedings.

Quick Common Legal Considerations in Cheque Dishonour Cases

FAQ's

Q1. What if I ignore a legal notice under Section 138?

You may face a criminal complaint. Court summons may follow, and repeated non-appearance can lead to a warrant.

Q2. Can a gift cheque or donation be prosecuted?

No. Only cheques issued against a legally enforceable liability attract Section 138.

Q3. Can civil and criminal cases be filed for the same cheque?

Yes. Criminal prosecution does not prevent a civil recovery suit under Order 37 CPC.

Q4. Can I file a complaint without serving notice?

No. A valid legal notice is mandatory. Without it, the complaint is not maintainable.

Q5. Can the accused be arrested in a cheque bounce case?

Not initially. It is a bailable offence. Arrest occurs only after repeated failure to appear in court.

Q6. What is the time limit to send a legal notice after the cheque is dishonoured?

You must send the notice within 30 days from the date you receive the return memo from the bank.

Q7. What if the cheque is returned due to technical reasons, like signature mismatch?

Even signature mismatch or account closure can be grounds under Section 138, provided other conditions are satisfied.

Q8. Is a scanned copy or photocopy of the cheque admissible in court?

Only the original cheque is generally admissible as primary evidence. However, certified copies may be considered in some cases if originals are lost and proper explanation is provided.

Q9. Can proceedings be initiated for partial payment cheques?

Yes, if the cheque represents part payment of a larger enforceable liability, proceedings can still be initiated for that amount.

Q10. What if the cheque was issued from a joint account?

Liability depends on who signed the cheque. If both account holders signed, both may be liable; otherwise only the signatory is considered.

Q11. Can the drawer deny receipt of the legal notice?

If the notice was properly addressed and sent by registered/speed post, courts may presume service. Refusal to accept delivery is treated as served.

Q12. What happens after a Section 138 complaint is filed?

The magistrate may take cognizance, summon the accused, and begin trial proceedings including evidence, cross-examination, and final arguments.

Q13. Can a complaint be filed in a different city from where the cheque was issued?

Jurisdiction lies where the cheque was presented for clearance, as per amended law post-2015.

Q14. Can the case be transferred to another city?

Only through court permission. Jurisdiction is typically fixed as per legal norms and cannot be changed without cause.

Q15. Can companies be prosecuted for cheque bounce?

Yes. Both the company and the person responsible for conduct of business (e.g., directors) may be named under Section 141 of the NI Act.

Q16. I gave a cheque as a security deposit, but the company encashed it and it bounced. Can I be prosecuted?

This is a common defence in cheque bounce cases. If the cheque was clearly issued only as a security and there was no legally enforceable debt at the time it was presented, you may have a valid defence. However, courts assess such claims based on supporting documents and circumstances. The burden lies on the accused to rebut the presumption under Section 139 of the NI Act.